26 March 2026

Savers have been losing money in real terms for 16 months in a row (up to February 2026), as cash ISA and instant access savings rates have fallen at the same time as inflation has gone up.

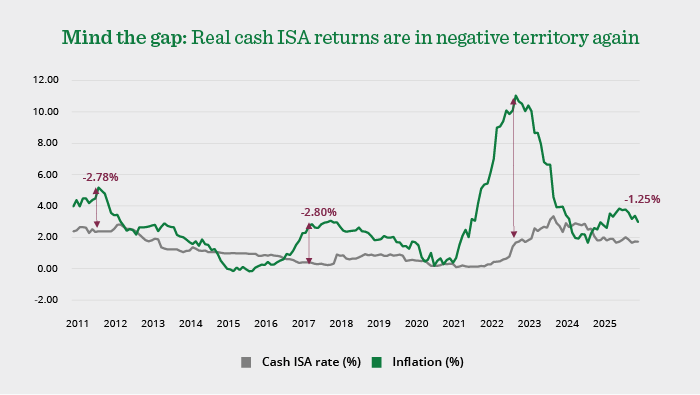

Analysis from Quilter shows that in February, CPI inflation was registered at 3.0%, down from 3.9% seen in July last year, nearly double the Bank of England’s 2% target, and its highest since January 2024.

But despite this fall in inflation, cash ISA rates have remained unchanged in that same period, with the monthly interest rates available on cash ISA deposits standing at, locking in a real term loss of 1.25%. Indeed, since October 2024, the last time average cash ISA rates provided a real return, those rates have declined by almost a third (32%). Even for an average instant access savings account, the real terms loss stands at 0.85% a year, with a positive return not being seen since December 2024.

Following the outbreak for increased geopolitical uncertainty, there are new fears that inflation may once again rise, despite hope it would return towards the BoE’s 2% target this year. While it’s hard to predict how things will move going forward, cash savings rates often lag changes to inflation and thus the gap in returns looks set to remain.

Even more startlingly, Bank of England data highlights that £300bn of savers’ cash is languishing in accounts that are paying no interest whatsoever, leaving savers themselves brutally exposed to the full effects of inflation.

Quilter in encouraging savers to take action on two fronts to help combat the cash gap:

- For any short-term and medium-term savings, make your cash work harder by using cash savings platforms that provide access to multiple providers in one place, allowing you to switch in and out of the best rates and lock in accounts above inflation.

- For any longer-term savings, cash ISA savers should consider a stocks and shares ISA. Investing generally offers better returns over saving and is more likely to keep pace with, and even exceed, inflation levels over the longer-term. Certainly, when compared to cash ISAs the rewards are clear.

Through Quilter’s CashHub, the best instant access savings rate is 3.61%, offering a real return of £61 for every £10,000 saved, compared to a real loss of £12.50 and £8.50 through an average cash ISA and instant access savings account respectively. Meanwhile, the best fixed term rate above three years available through the CashHub currently stands at 4.10%, offering the chance to lock in a real return of 1.1% compared to today’s inflation rate.

Meanwhile, someone who invested £10,000 in a cash ISA in January 2011 would currently have £12,214.75. Adjusted for inflation, this is just £7,785.16. In contrast, a £10,000 investment in a stocks and shares ISA, held in the IA Global Equity index over the same period would be worth £36,856.35 or £23,515.67 after inflation. These figures do not account for charges that may reduce the final sum.

Holly Tomlinson, financial planner at Quilter, commented:

“For well over a year now, savers have been hit by the scourge of inflation as cash savings rates have lagged inflation and look set to for the foreseeable future. People putting their money into these savings accounts are, more likely than not, to be locking in real term losses, reducing their money’s future value.

“Savings rightly play a key role in people’s finances. They offer good short- and medium-term options to park your money, but if you are to make the most of it then people need to be active. The good news is there are options available. Cash savings platforms offer an easy way to get access to above inflation rates, allowing you to seamlessly manage your money in real time across a number of providers, ensuring you are getting the best rate out there, while benefitting from the likes of FSCS protection.

“There are a number of savings accounts out there that are beating inflation, so the options are there for savers in the short- and medium-term, they just need to take action.

“Meanwhile, in the longer-term people need to be prepared to put their money to work by investing for five years or more. This has proven to be the best way to beat inflation over the long-term consistently. Saving and investing can co-exist happily as part of someone’s overall financial situation. So long as you are managing the risk that inflation presents that is the most important action someone can take.”

Holly’s tips for beating inflation:

- Make your cash active: Finding the best savings rates can be a tiresome task, with various bonuses being offered and many rates being at the whim of the overall BoE interest rate. Use a cash platform to help manage your short-term savings, giving you access to a wider variety of providers at inflation-beating rates.

- Diversify, diversify, diversify: The first rule of investing is to diversify your portfolio to reduce the risk. For example, by buying a range of shares and having a diverse asset allocation including bonds, property and alternatives.

- Understand what you are investing in: The investment universe is enormous and growing at a rapid rate. It is important to know exactly what you are buying, what the return drivers are and what the risks are.

- Have a realistic plan: Investing is a marathon, not a sprint. You need to know how much you can realistically set aside each month to invest, understand your capacity for loss, and get exposure to a suitable amount of risk given your investment objectives.

- Watch out for red flags: When inflation is high, people often turn to social media for tips or too good to be true offers. Be wary of a savings account or investment that offers an unrealistic rate of return, which downplays the risks or puts you under time pressure to make a decision. If in doubt, check the FCA’s register and make sure you a dealing with a regulated financial services firm. For more information visit https://www.fca.org.uk/scamsmart.