16 October 2023

Investors sitting in cash risk missing out on significant market gains if the end of the rate hiking cycle has been reached, according to wealth manager and financial adviser, Quilter.

At its last meeting of the Monetary Policy Committee, the Bank of England held interest rates at 5.25%, with speculation that the end of the interest rate hiking cycle is over.

There is now mounting assumptions that the Bank of England will cut rates at some point in 2024, particularly given the uncertain economic environment facing the UK.

If that were the case, Quilter has found that in previous cases when the Bank of England has cut interest rates following the end of the rate hiking cycle, returns have been particularly strong in the year after.

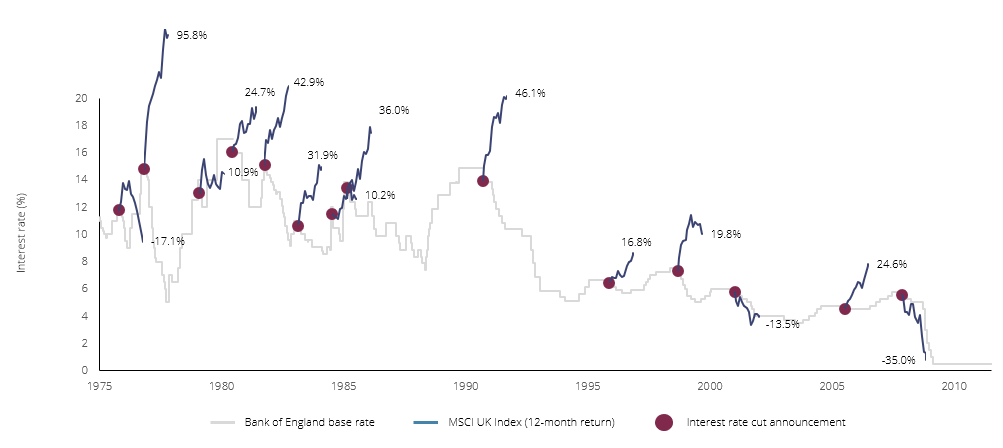

For example, following the first cut in rates in 1990s, the MSCI UK Index returned 46.1% over the next 12 months. Remarkably, in 1976 after interest rates were cut from 15% the UK market subsequently rose 95.8%. While not all moves are as extreme and some periods were impacted by global events, the data clearly highlights that the market reaction is strongest in the early part of a rate cutting cycle.

1 year returns after the first cut in interest rates following series rate hikes

Source: Quilter Investors

This is also not just exclusive to equities. For example, a 10-year gilt bought at a yield of 4.8% would generate a return of approximately 13% if the yield on the bond fell by 1%, highlighting the power any interest rate cut is likely to have for those remaining invested in the market.

Conversely, as interest rates are cut, interest rates offered by the banks are likely to fall too, meaning those with assets sat in savings accounts will see an immediate drop in their returns as banks look to take advantage of falling borrowing costs for themselves.

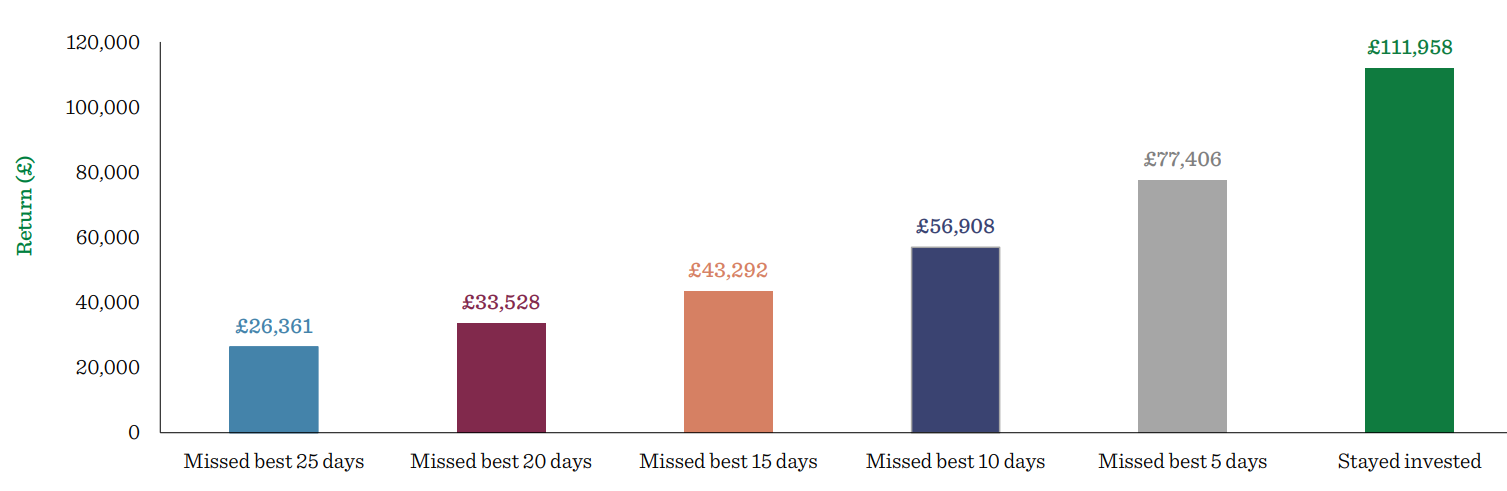

Quilter is stressing to investors the benefits of staying invested regardless of where cash rates sit today. The chart below shows that missing just the 10 best days in the market could result in your investment being almost halved in value compared to remaining invested in the stock market.

Source: Quilter Investors as at 30 June 2023. Total return over period 30 June 1993 to 30 June 2023 based on initial investment of £10,000 into the MSCI All Country World Index.

Lindsay James, investment strategist at Quilter Investors, said: “For most people, cash feels like a safe place to be, and with rates where they are at the moment, many have taken the decision to take 4% or 5% per year with what appears to be very little risk. However, there are a couple of things at play here that suggest sitting in cash isn’t quite as risk free as people thought.

“The first should be well known by now and that is inflation. Put simply, inflation erodes the value of your cash. And with the headline rate of inflation still considerably higher than most savings accounts, people sitting out of the stock market are losing money in real terms.

“The second thing to consider is the reinvestment risk. When the Bank of England does come to cut interest rates, savings rates will be the first to be brought down and immediately your return is slashed. Furthermore, cuts to interest rates are likely to act as immediate stimulants to financial markets and thus if you are sat in cash, you will likely miss out on the best days – something that can cost you significantly in the long-run.

“Missing out on the recovery, which is often where the best returns can be made, can considerably impact the value of your pot when it comes to utilising it. This will also impact those in fixed-term savings deposits, who have no choice but to miss out on any market recovery that does take place.

“The warning signs are clear for investors. Investing is a long-term game, but it is one that gives you the best opportunity to grow your wealth in real terms regardless of inflation. Cash may seem like a safe asset to hold but have too much of it at your peril.”